")

Arbitrage tactics uses the difference in the rate of change in demand for specific trading assets. Forex arbitrage strategies work reliably in any market, as they give the possibility of earning directly from the movement of prices, regardless of the direction and strength of the expected trend.

First arbitrage transactions appeared on commodity and stock exchanges; this technique gives significantly lower results on the foreign exchange market, but today it is the one that helps hedge funds to avoid major losses during prolonged trends.

Forex arbitrage strategies base on trading models reflecting the inefficiency of pricing on certain financial assets – the investors will be interested in any imbalance in the price behavior. Arbitrage result depends only on the rate of change in prices. Techniques provide a mixed current analysis on several trading instruments at a time: stocks, currencies, futures. Let’s consider the most popular arbitrage strategies available to almost every trader.

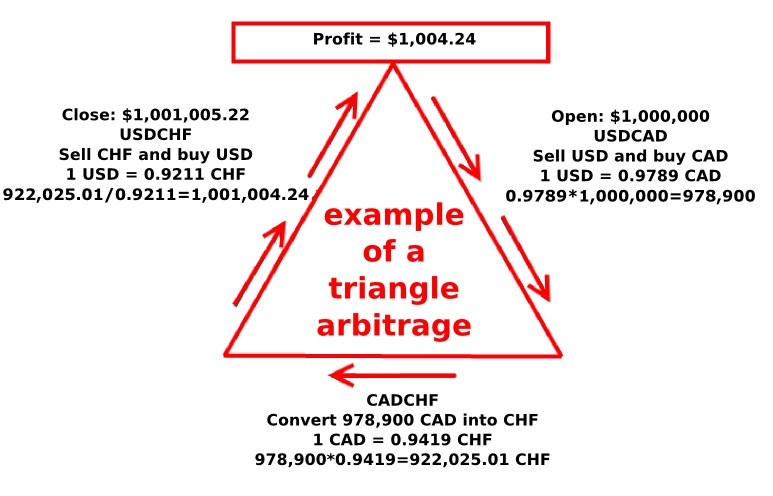

Triangle strategy

The technique: trading is conducted on three currency pairs in order to "catch" the difference between the actual price and artificial (synthetic) rate. For tangible yield, you need a fairly wide spread and the real delay of the price across the transaction participants. We act in three steps under such a scheme:

- deal with the currency A (USD) through the currency B (CAD);

- deal with the currency B (CAD) through the currency C (CHF);

- deal (reverse) with the currency C (CHF) through the currency A (USD);

Important: yield on this strategy is very sensitive to even minor unaccounted negative factors.

Benefits: substantial and fairly fast profits at large investments, the possibility of earning on the implicit (unstable) market, low risk at constant analysis and rapid response to the situation.

Strategy of interbourse (intermarket) arbitrage

Just note that these Forex arbitrage strategies do not include the "game" on the difference in the quotations of brokers, which arises from the standard technical reasons or as a result of failures.

We remind that Forex is the interbank spot market, where, in addition to currency pairs, currency futures with their individual dynamics also operate.

From time to time, there is a possibility of earning on the exchange rate difference between the futures and currency by opening opposite transactions in different markets. The largest difference occurs in the days of futures expiration or before the fundamental news. DCs with low spreads and commissions, and capital from $500 are sufficient for such transactions.

Trading strategy on correlations or spread trading

We remind that in this context, the term "spread" is not the difference between the ask/bid prices, but the price difference between the two (or more) trading assets.

There are many indicators of spread differences, but the modifications of the dollar index, which you can easily edit in MetaEditor, are the most commonly used. In this example of Forex arbitrage strategies, the mutual "spread" on currency pairs usdx/usdsek will reduce, provided that:

- US dollar depreciates faster;

- Swedish krona appreciates faster (compared to the US dollar);

- US dollar appreciates slower (compared to the krona).

Due to the high cross-correlation, such "spread" most of the time remains in the range with the recurrent test of boundaries. After the synthetic rate rebounded from the range and began to move in a certain direction, you need to buy usd/sek and sell usdx. The transaction is better to close automatically (by script or expert advisor).

Separate kind of Forex arbitrage strategies is trading with "calendar spread", where the asset with a nearest closure term (futures on assets) is bought (or sold) and the more distant contract is sold (bought).

Statistical arbitrage and paired trading

The strategy consists of the simultaneous opening of the transactions on (at least) two currency pairs with a strong cross-correlation. After determining the target pairs with a strong direct or inverse correlation, it is necessary to constantly monitor the correlation value and when there is a deviation from the equilibrium level, you need to buy the weakest pair and sell the strongest, i.e. use the non-uniform acceleration of price movement. The basic concept is a "synthetic" currency pair. NZD/USD and USD/JPY pairs can be considered an example of a direct correlation.

Pairs move synchronously, but with different acceleration. The synthetic pair is NZD/USD*USD/JPY= NZDUSD/USDJPY (real counterpart is a direct NZD/JPY cross).

The real exchange rate of the cross-pair shows an "equilibrium" value of the synthetic pair, i.e. entering the market means selling NZDUSD/USDJPY. Since the correlation between the component pairs is direct, two-way deals are opened on them: buy NZD/USD and sell USD/JPY. Closing occurs when the rate of synthetics coincides with the real exchange rate of NZD/JPY. The size of the profit from this type of Forex arbitrage strategies is the difference of the rates of the synthetic pair and cross-rate minus two spreads.

For pairs with a reverse correlation we argue similarly, except that the transactions are opened in one direction (either two buys or two sells).

There are situations when the rate of change of one component pair does not compensate for the speed of the second, or when there is a powerful news surge on one of the pairs, so the current control of the correlation is required.

Important: even if one component pair – for example, USD/JPY – gives a strong trading signal, be sure to open the transaction on the second pair to minimize the overall risk on arbitrage transactions.

Exotic Forex arbitrage strategies

Arbitrage hedging

It is understood that the transactions will be long, so the size of the swap plays a large role. Usually two (or more) accounts are opened with different brokers, one of them must be swap-free, and on the other you need to choose a currency pair with a positive swap. After that, transactions of the equal volume are opened on both accounts, but in different directions, and wherever the rate goes, you can at least get profit from the swap. You can close simultaneously in both positions or only on unprofitable ones.

Network (or territorial) arbitrage

With the development of high-speed communication channels, the attempts to use the difference in the rates on various exchanges and mismatch of quotes of various brokers is almost never used, but there is an example of currency pairs that are suitable for this technique: EUR/USD and EUR/HKD. Hong Kong’s currency regulation obliges to peg the current exchange rate of the national currency to the US dollar, so there is a recurring short-term difference, which can be caught in between the adjustments of exchange arbitrageurs at the beginning and end of the session.

And as a conclusion...

- If you are going to trade under the Forex arbitrage strategies, do not focus on the fast transactions. The best initial timeframe is D1.

- Most often two spreads are paid, i.e. you need brokers without slippage and with minimal spreads (possibly floating).

- Start arbitrage trading with small volumes and assets with a high long-term correlation.

- Always hedge the major currency rather than the minor and choose different news providers for different assets. For example AUD/USD and AUD/JPY are not beneficial for the mutual arbitrage, while silver and gold fit well.

Arbitrage usually has a small profitability, which requires frequent transactions, but sometimes it can be very volatile, so do not let the current drawdown of more than 20%. Its judicious application allows to save (and sometimes increase) a deposit in an uncertain market. Source: Dewinforex